Narrative Alpha: Hivemind's Emergent Broad-Market Signal

Our narrative factor attempts to capture performance drivers similar to the momentum factor, but instead of chasing a symptom, it chases the root cause - growing market-relevant narratives driving changes in expectations and prices.

We are excited to share preliminary results from our narrative factor alpha benchmark.

Applying a naive, systematic implementation of Hivemind's narrative factor within a S&P 500 proxy universe, our backtest achieves:

- a 1.0x IR in an industry-neutral, top minus bottom decile portfolio, and

- a 0.9x IR in a subindustry-neutral, top minus bottom decile portfolio.

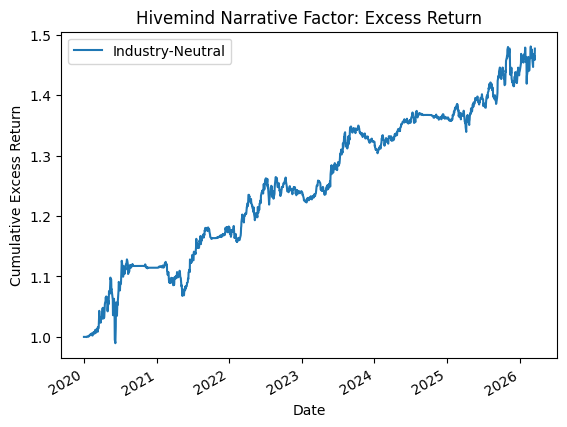

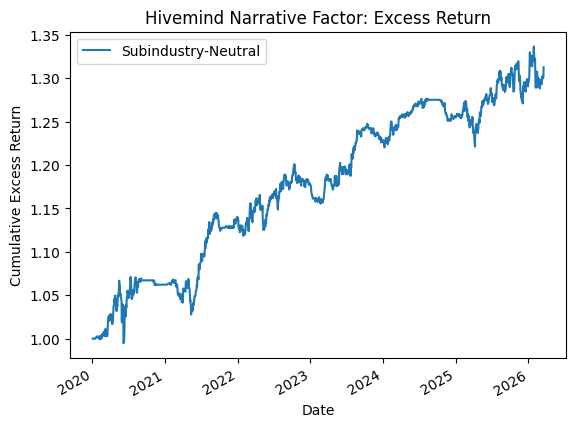

Preliminary Backtest Results

Industry-Neutral

# Initial date 2020-01-02

# Final date 2026-03-18

# Annualized excess return (%) 6.49%

# Annualized excess risk (%) 6.42%

# Information ratio (x) 1.01x

# Max drawdown (%) 9.89%

# Max daily turnover constraint (% AUM) 3.00%Subindustry-Neutral

# Initial date 2020-01-02

# Final date 2026-03-18

# Annualized excess return (%) 4.48%

# Annualized excess risk (%) 5.03%

# Information ratio (x) 0.89x

# Max drawdown (%) 6.74%

# Max daily turnover constraint (% AUM) 3.00%The above backtests, built and run using our open-source solution ForecastOS PM, exclude transaction costs and short holding costs.

Turnover is ~3.5x (two-way) per year, or roughly 1.75x per (long and short) side.

Hivemind's Narrative Factor: What is Being Measured

Our narrative factor attempts to capture performance drivers similar to the momentum factor, but instead of chasing a symptom (i.e. previous returns which may indicate the presence of a positive tailwind), it chases the root cause - growing market-relevant narratives driving changes in expectations and prices.

The Hivemind narrative factor blends discussion-weighted Hivemind exposures related to point-in-time market relevant narratives within 95% of their trailing 6-month discussion highs.

The result is a new factor that is broadly applicable and that works on a medium to long-term timeframe.

You will notice a couple of short horizontal lines in the above excess return evolution. Those correspond to brief periods when there were no market-relevant, investable narratives within 95% of their 6-month discussion highs. Said another way: the Hivemind narrative factor is a weighted composite of transient narratives and associated exposures; occasionally, no market relevant narratives near trailing highs exist.

Hivemind's Narrative Factor: Why it Matters

While preliminary, the results are unusually strong given the liquidity and efficient pricing of the S&P 500 universe. Further, all else equal, increasing breadth should increase IR.

While more research and proof of value is due, we're excited by what we've seen to date!

Accessing Hivemind's Narrative Factor and Backtest

ForecastOS Hivemind clients have access to the code and methodology used and discussed above, including the portfolio construction framework, narrative factor construction / eligibility rules, and performance measurement approach used in these preliminary results.

Clients can inspect exactly how the benchmark is built, reproduce the process end to end, and adapt the implementation to their own research, universes, and deployment constraints. Our goal is not just to show the results, but to make the benchmark transparent, testable, and directly usable as a foundation for live investment workflows.

If the above is of interest to you, email us at [email protected] to schedule a call. We'd love to show you what we've built and how you can integrate it into your research and investment process.

Note: associated white paper to come.