Months of Hard Work. Three Updates

Welcome to Weekly Roundup #19 at ForecastOS! We're glad to have you here, following our journey :)

We've been quiet for the last three months, hard at work on:

- A ML-driven, market neutral quant investment strategy

- Our open-source portfolio optimization and backtesting framework, InvestOS

- A fundamental financial dataset for US equities

1. A ML-driven, market neutral quant investment strategy

In January, we realized that we needed an internal systematic investment strategy to better iterate on and improve our portfolio optimization and backtesting framework, InvestOS.

So we got to work.

We created (A) +1300 alpha and risk factors (available in ForecastOS), which we used to create (B) return forecasts, which we used to (C) create, optimize, and backtest market neutral portfolios with simulated slippage / trading / holding costs.

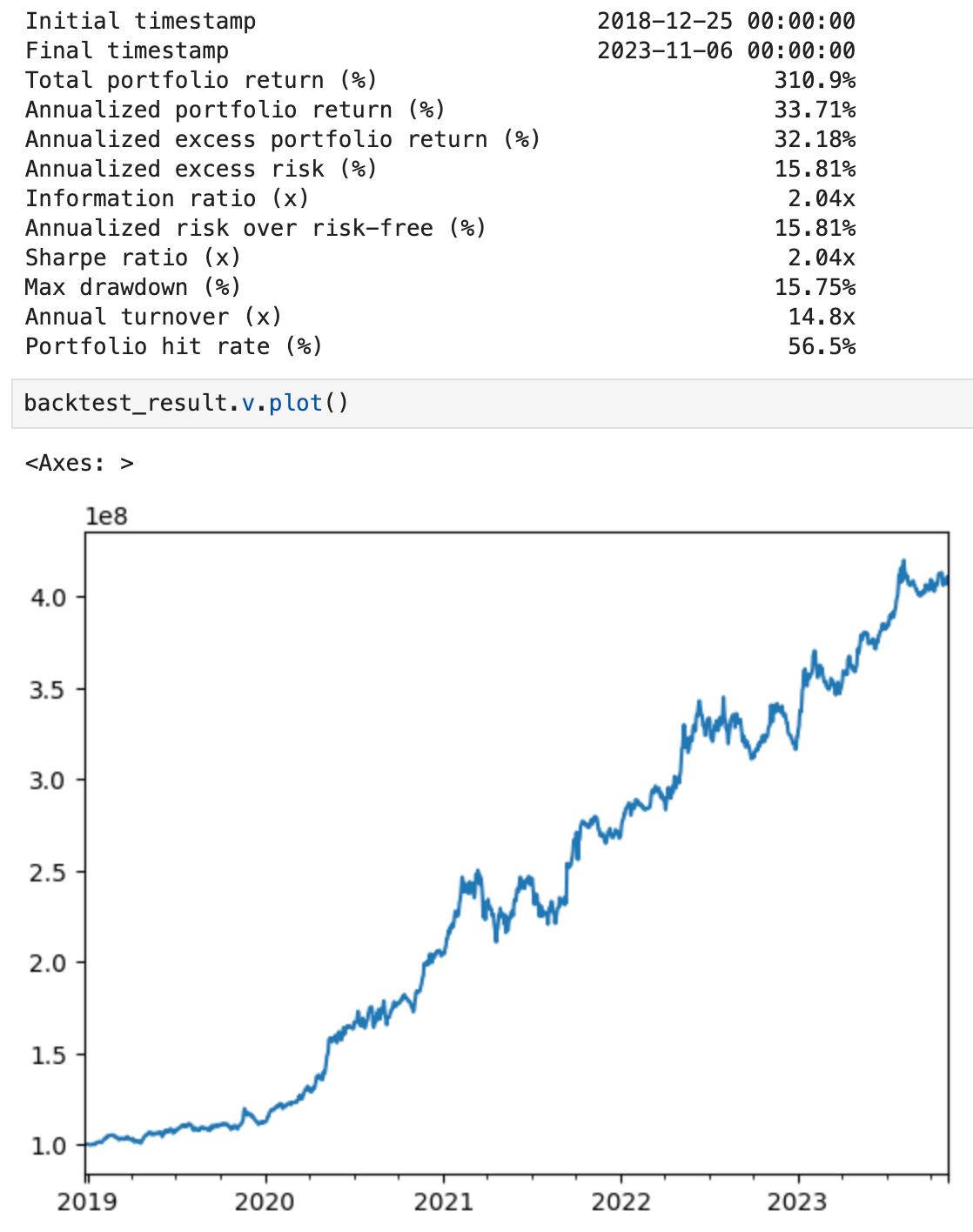

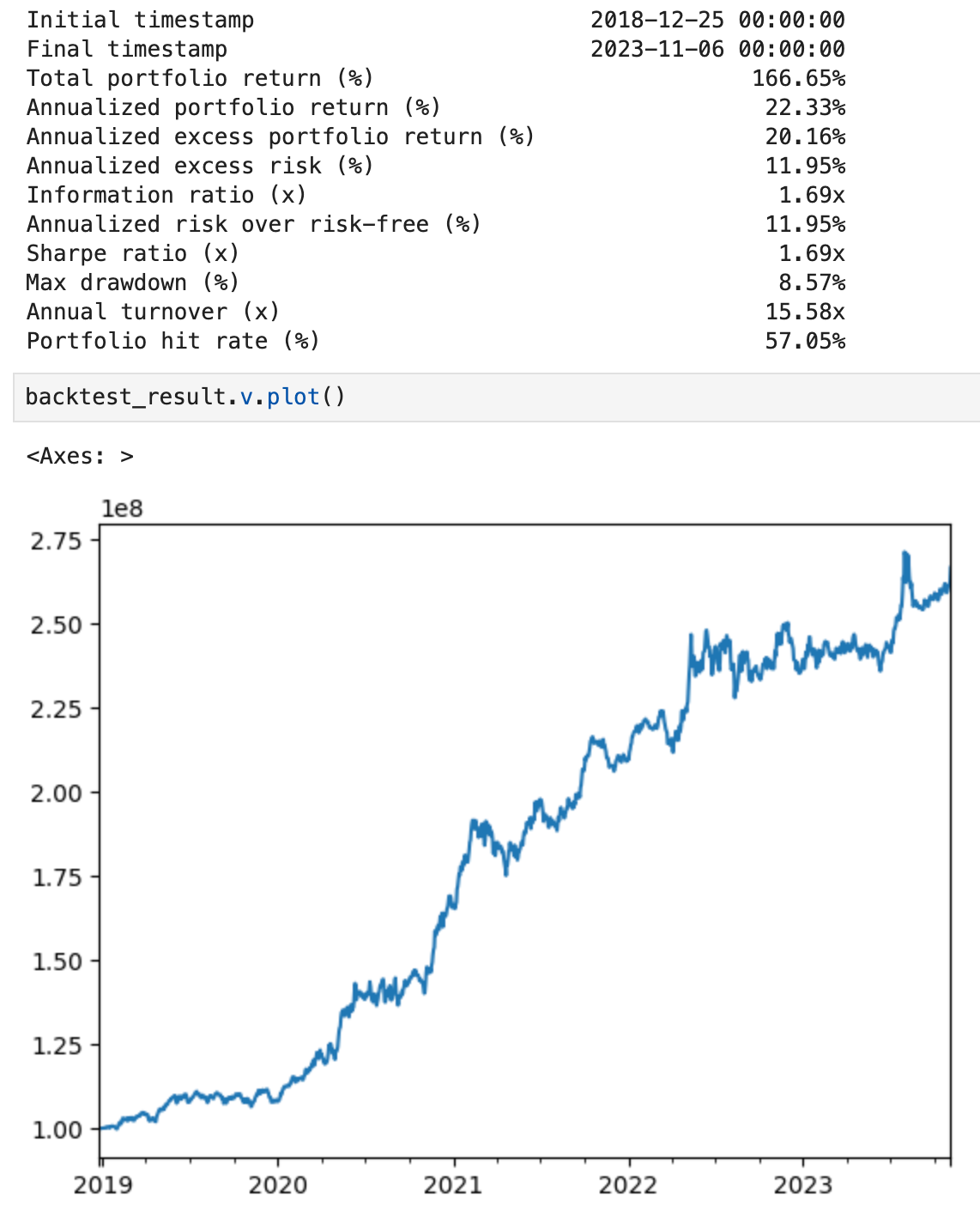

An InvestOS backtest screenshot from our internal market neutral strategy can be seen below.

We also created a (similar) strategy that builds tranches of optimized portfolios using our SPOTranches class. In addition to being market neutral, it is industry, size, momentum, and leverage neutral. It has slightly worse risk-adjusted performance, but due to its constraints, better drawdown characteristics.

2. Our portfolio optimization and backtesting framework, InvestOS

As you may have gathered from the above: we're investing a lot of time into improving our portfolio engineering and backtesting framework, InvestOS.

Expect updated guides, new constraint / risk models, and (free) performance attribution functionality in the next several releases.

3. A fundamental financial dataset for US equities

Data has been a growing obsession of mine over the last ~4 years. It's one of the few inputs required to create AI that feels like magic.

If you REALLY know me, you also know that I used to spend countless hours reading, understanding, and analyzing information contained in public company financial filings. I remember the constant hunt for weird debt covenants, obscure minority and equity interests, and buried EBITDA add-backs (always check the footnotes!). As a former investment banker, 20% of my perceived self-worth came from my ability to sleuth out fringe financial information and model it appropriately!

Fortunately, these two areas of interest are colliding.

We're preparing to launch a new financial dataset for US equities SOON!

Stay tuned.

Work: What's Coming Next

We now have a lot of exciting things to show our fellow investors. That's what we're focused on next: connecting with institutional investors.

As such, if anything we said above was interesting to you, or you know someone we should connect with, shoot us an email at [email protected]!

We'd love to show you everything we've cooked up :)

Until next week,

Charlie